Addressing shortfalls, modernising resolutely

EXECUTIVE SUMMARY

Click to share

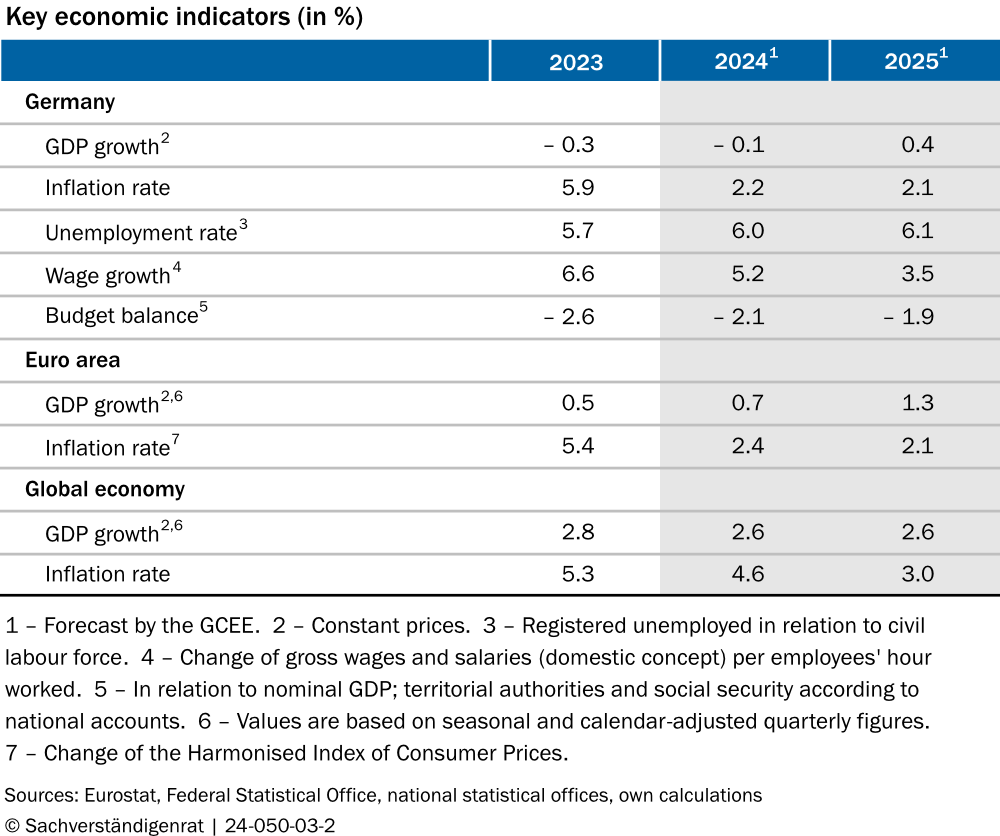

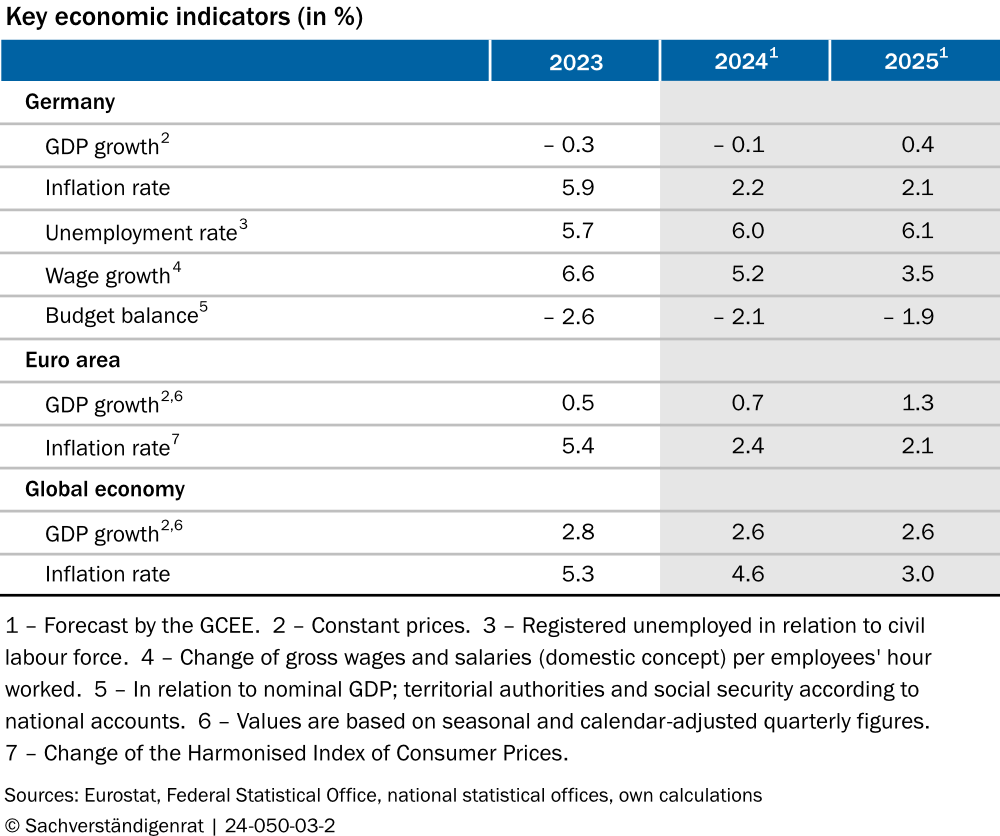

(1) The German economy continues to stagnate. Gross domestic product (GDP) has grown by only 0.1 % overall in real terms over the past five years. Germany's potential output is more than 5 % below the 2019 estimate for potential output in 2024. In terms of GDP growth, Germany clearly lags behind other advanced economies. This suggests that the German economy is being held back by both cyclical and structural problems. ITEM 24 Although energy prices have fallen significantly following the energy crisis, they have stabilised above the level seen before the COVID-19 pandemic. ITEM 44 Real incomes have recovered from the income losses in the wake of high inflation between autumn 2021 and mid-2023, but consumption is not picking up and the savings rate remains high. ITEMS 51 F. In manufacturing, competitiveness vis-à-vis key trading partners has continued to decline and there are no signs of improvement. ITEMS 45 F. Capacity utilisation and labour productivity have also declined. ITEM 42 BOX 7 The German economy is therefore expected to grow only slightly in the coming year and to continue lagging well behind the other advanced economies.

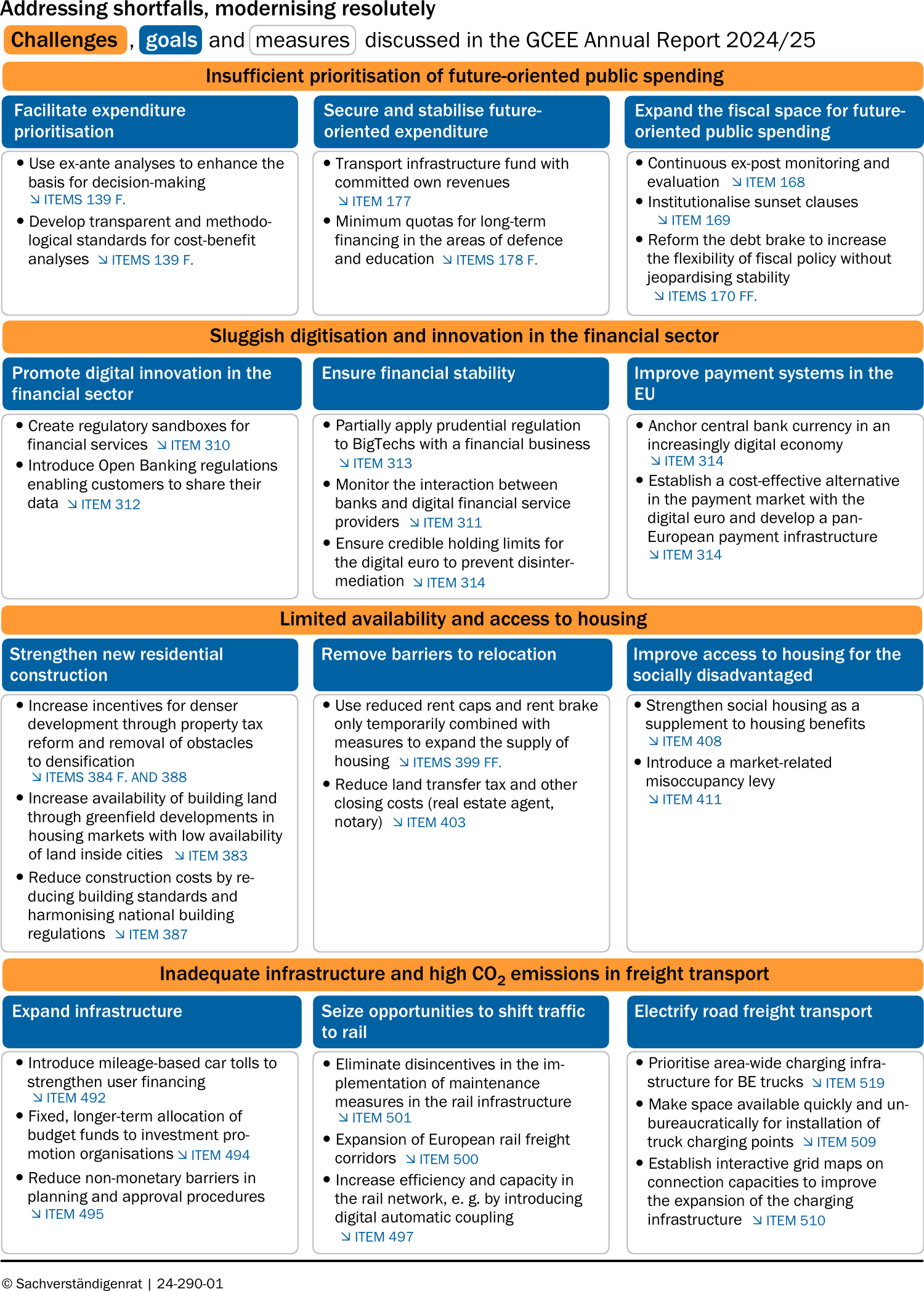

In addition to the discussion of the current and forecast state of economic activity, particularly in manufacturing, this report analyses four other areas in which Germany has failed to resolutely take a path towards modernisation. CHART K1 First, future-oriented public spending must be better prioritised, secured by binding commitments. Spending on infrastructure, education and defence is low by international standards, and significant shortcomings have emerged in recent years. Second, transport infrastructure needs to be modernised and freight transport needs to be decarbonised. Third, Germany is lagging behind in the digitalisation of the financial system and is therefore missing out on potential for innovation and efficiency gains. Fourth, the housing market is particularly tight in urban areas. This makes it difficult for labour to move to productive regions, and at the same time, the rent burden is very high in these regions, affecting especially socially disadvantaged households.

- Use ex-ante analyses to enhance the basis for decision-making Items 139 F.

- Develop transparent and methodological standards for cost-benefit analyses Items 139 F.

- Transport infrastructure fund with committed own revenues Item 177

- Minimum quotas for long-term financing in the areas of defence and education Items 178 F.

- Continuous ex-post monitoring and evaluation Item 168

- Institutionalise sunset clauses Item 169

- Reform the debt brake to increase the flexibility of fiscal policy without jeopardising stability Items 170 FF.

- Create regulatory sandboxes for financial services Item 310

- Introduce Open Banking regulations enabling customers to share their data Item 312

- Partially apply prudential regulation to BigTechs with a financial business Item 313

- Monitor the interaction between banks and digital financial service providers Item 311

- Ensure credible holding limits for the digital euro to prevent disintermediation Item 314

- Anchor central bank currency in an increasingly digital economy Item 314

- Establish a cost-effective alternative in the payment market with the digital euro and develop a pan-European payment infrastructure Item 314

- Increase incentives for denser development through property tax reform and removal of obstacles to densification Items 384 F. and Item 388

- Increase availability of building land through greenfield developments in housing markets with low availability of land inside cities Item 383

- Reduce construction costs by reducing building standards and harmonising national building regulations Item 387

- Use reduced rent caps and rent brake only temporarily combined with measures to expand the supply of housing Items 399 FF.

- Reduce land transfer tax and other closing costs (real estate agent, notary) Item 403

- Strengthen social housing as a supplement to housing benefits Item 408

- Introduce a market-related misoccupancy levy Item 411

- Introduce mileage-based car tolls to strengthen user financing Item 492

- Fixed, longer-term allocation of budget funds to investment promotion organisations Item 494

- Reduce non-monetary barriers in planning and approval procedures Item 495

- Eliminate disincentives in the implementation of maintenance measures in the rail infrastructure Item 501

- Expansion of European rail freight corridors Item 500

- Increase efficiency and capacity in the rail network, e.g. by introducing digital automatic coupling Item 497

{kind=link}

{kind=link}

1. Growth is still not picking up

(2) Economic development in Germany remains persistently weak, primarily due to a decline in industrial production and value added in manufacturing. ITEM 41 By contrast, the global economy and global industrial production are experiencing positive growth rates. Global GDP is expected to grow by 2.6 % both in 2024 and 2025. ITEM 13 The euro area is expected to grow by 0.7 % and 1.3 %, respectively. CHART K2 ITEM 30 The decoupling of the German manufacturing sector from the global economy indicates that the German weakness is not only cyclical, but also has structural causes.

(3) The weakness of German manufacturing is likely to reduce the willingness to invest in the manufacturing sector and to adversely affect business services. ITEMS 47 AND 59 Also, the weak German economy increasingly affects the labour market. Growth in employment has almost come to a standstill and the unemployment rate has risen by 0.3 percentage points since August 2023. The increase in unemployment was above average in manufacturing and construction, sectors which are particularly affected by weak growth. ITEM 65 Despite significant increases in real wages in the current year, households have not yet increased their consumption expenditure. ITEM 51 Given high uncertainty about future economic development and slowing real wage growth, consumer demand will likely continue providing only weak impulses for growth in the forecast period. ITEMS 43 AND 59

{kind=link}

{kind=link}

{kind=link}

{kind=link}

(4) The German Council of Economic Experts (GCEE) expects real GDP to decline by 0.1 % in 2024. It is thus revising its forecast downwards by 0.3 percentage points compared to spring 2024. In 2025, it expects only slight growth of 0.4 %. ITEM 40 BOX 5 Inflation is expected to average at 2.2 % in 2024, 0.2 percentage points lower than forecast in spring 2024. The inflation rate is expected to be 2.1 % in 2025. CHART K2 Core inflation is expected to be 3.0 % in 2024 and 2.6 % in 2025. ITEM 64 Downside risks to the forecast for the German economy include a deeper weakening of industry ITEM 72 and a further increase in uncertainty, which could dampen investment and private consumption more than expected. These effects could be exacerbated if slower growth renders additional reductions in public spending necessary. Vice versa, a more positive development could emerge if the reluctance of private households to consume disappears and the saving rate normalises more quickly than expected. ITEM 75

2. Strengthening the future-orientation of public finances

(5) In Germany, future-oriented public spending has been low for years. ITEMS 91 FF. Investments and expenditures with high costs today and returns only in the distant future have been too low, especially compared to other European countries. CHART K3 There has been a failure to prioritise public spending for key areas such as transport infrastructure, defence and the education system, and the resulting shortfalls have become apparent in recent years. For example, public investment in civil engineering, which mainly concerns public transport infrastructure, has been insufficient for decades to maintain the existing infrastructure. ITEMS 98 F. Germany’s outdated infrastructure significantly restricts freight and passenger transport and hampers economic development. BOX 28 In the defence sector, both a spending increase and a more efficient use of funds are needed to modernise equipment and meet NATO's spending target. ITEM 108 When it comes to education, Germany is performing worse than ever in international comparative studies, and the insufficient funding for early childhood education and primary education is likely one of the primary reasons.

(6) Various obstacles stand in the way of higher and more continuous future-oriented public spending. The competition for votes often leads to a present bias in politics. That is, policymakers often prioritise expenditures that benefit the current electorate over expenditures that will only yield a return in the future. ITEMS 119 FF. Fiscal rules designed to restrict borrowing can preserve the fiscal space of future generations, but they do not ensure an adequate prioritisation of expenditures. ITEMS 131 FF. With fiscal space becoming increasingly tight, there is further risk that future-oriented expenditures will be reduced. ITEMS 124 FF. In addition, bureaucratic obstacles in the form of complicated permit processes and understaffing of the public administration are likely to inhibit future-oriented public spending. ITEMS 134 FF.

(7) In order to increase and stabilise future-oriented public spending, institutional provisions are needed that counteract the present bias of politics. ITEMS 142 FF. A DIFFERING OPINION ITEM 180 To this end, the GCEE analyses the design of provisions that could ensure a high degree of commitment. The focus on prioritisation distinguishes the analysis presented here from numerous earlier proposals that focus on options for expanding the scope for using debt to finance public investment. Suitable provisions must be tailored to the respective area of expenditure, taking into account in particular (1) whether it is a one-off or a permanent increase in expenditures, (2) how clearly the expenditure can be delineated and separated from other areas of investment and spending, and (3) which level of government (federal, state or municipal) is responsible for financing and implementation.

(8) There exists a considerable backlog in the modernisation of transport infrastructure. Spending on infrastructure investment and maintenance should be permanently increased and stabilised. At the federal level, an intermodal transport infrastructure fund would make for a suitable instrument to finance that spending. ITEM 177 A DIFFERING OPINION ITEMS 206 F. In order to credibly stabilise spending on transport infrastructure, the fund should be endowed with own revenues and could be included in the German constitution (Basic Law). To this end, revenues from the truck toll and from a new car toll (which should replace the energy tax on fossil fuels in the transport sector, as its revenues will be declining) could be transferred to the fund. A transfer of revenues from the energy tax on fossil fuels in the transport sector or the motor vehicle tax could also be considered. Transferring revenues from the core budget ensures that the establishment of the fund does not increase the available fiscal space for present-oriented expenditure in the core budget. ITEMS 146 F. In light of the backlog of investment in the transport infrastructure, the fund could also be endowed with limited credit authorisations. ITEM 150 These should be subject to the limitation of the debt brake, for which the GCEE proposes a stability-oriented reform. ITEMS 170 FF. AND 177 A DIFFERING OPINION ITEM 210 Providing credit authorisations would help smooth out cyclical fluctuations in the fund's income.

(9) In the area of defence, the lengthy procurement processes should be simplified and the efficiency of the use of funds increased. ITEM 134 In order to ensure the long-term financing of national defence, NATO’s two percent target could become a statutory minimum quota. ITEM 178 A statutory minimum quota would also be suitable for education spending by the federal states. Such a quota should take demographic components into account, for example by requiring a minimum expenditure per pupil. ITEM 179 The exact design of the quota must account for the responsibilities of the federal government, federal states and local authorities for funding and implementation.

3. Seizing the opportunities of digital finance

(10) The digital transformation in the financial sector amounts to far more than a shift from traditional to digital products, as we see already in the payments market, for example. CHART K4 TOP It is a structural change, with new players entering the market who challenge incumbents in activities such as payment services, broker services and, increasingly, lending. CHART K4 BOTTOM These new players include specialised digital financial service providers (FinTechs) as well as large technology companies (BigTechs) that are expanding into financial services. At the same time, the European Central Bank plans on positioning itself more strongly in the digital payments market with the envisaged digital euro. ITEMS 283 FF.

(11) For households and firms, who are the users of financial services, digitalisation largely offers opportunities, in particular lower costs. Services are provided more efficiently, e.g. by implementing automated processes and using digital data. ITEMS 256 FF. In addition, increased competition reduces the market power of incumbents. There are opportunities for cost reductions in payment services, for example, where merchants still pay high fees. BOX 17 Furthermore, digitalisation improves customer convenience, ITEM 259 as access to financial services is eased and processing times are shortened. New products (e.g. through neo-brokers) also become available. ITEMS 260 FF.

However, the digital transformation creates risks and new challenges for bank and financial regulation as well. Differences in regulation between banks and FinTechs or BigTechs or differences in the application of common European regulations by national supervisory authorities may open up arbitrage opportunities, resulting in business being shifted to less regulated areas. ITEMS 288 F. Stability risks could also arise if the digitalisation of the financial sector increases the likelihood of abrupt liquidity outflows from the banking system ITEM 299 or if banks take higher risks when faced with declining margins. ITEMS 297 F. However, such risks to financial stability from the digital transformation are currently likely to be limited in Germany. This is primarily due to FinTechs and BigTechs playing only a minor role in core segments of the German banking market (e.g. lending). CHART K4 BOTTOM

(12) The main challenge for economic policy makers is to enable digital innovation in the financial sector in order to realise efficiency gains and quality improvements and at the same time ensure financial stability and avoid systemic risks. Limited regulatory sandboxes for new providers and products can foster innovation. ITEM 310 In addition, Open Banking regulations that enable customers to share their financial data across providers at the customer's request can contribute to a level playing field for all financial services providers. ITEM 312 The digital euro could offer a cost-effective alternative to private payment service providers and help establish an autonomous, pan-European payment infrastructure. ITEM 314 The design of the digital euro should include holding limits which would prevent massive outflows of customer deposits from banks and thus greatly reduce risks to financial stability.

4. Expanding housing supply with an eye on social hardships

(13) In Germany, there has been a steep increase in house and rental prices over the past 15 years, particularly in urban areas. ITEMS 323 FF. During this period, demand for housing has risen sharply in urban areas and economically strong rural regions. ITEMS 326 FF. The increase in demand is partly due to an increase in the share of single-person households, which require more space per person, and partly due to strong population growth, which is attributable to immigration and is concentrated in urban areas. In contrast, the supply of housing in urban areas has not expanded enough, particularly due to insufficient land availability and a lack of construction activity. ITEMS 350 FF. At the same time, a significant share of housing remains vacant in rural and economically weaker regions. ITEMS 351 Concurrent with increasing prices, the gap between rents agreed in new contracts and rents under existing contracts has widened significantly due to government regulations. The gap is particularly large in the tight housing markets of urban areas. CHART K5

(14) For urban areas with tight housing markets, the main challenge is to provide more housing. ITEMS 348 FF. The low availability of housing in urban areas can restrict access of workers to productive companies and labour markets. This implies that labour is not allocated to where it is most productive, resulting in efficiency losses. In particular, scarce building land, high regulatory requirements and high construction costs inhibit the construction of new housing in urban areas. ITEMS 345 FF. At the same time, housing in neighbouring regions takes little pressure from urban areas due to inadequate transport connections. Moreover, existing housing is often utilised inefficiently. People increase their living space as their family size and income increase, but do not reduce it once the children have moved out. ITEM 355 The main barriers to relocation are social, such as attachment to one's own home and to a familiar social environment. ITEM 356 However, financial barriers, such as the difference between existing and new rents and high transaction costs, also distort the incentives for efficient housing utilisation. ITEMS 357 FF.

The second central challenge of housing policy is to provide adequate access to housing. ITEM 366 FF. Due to the short supply of housing and the resulting high rents and real estate prices in urban areas, access to housing is particularly limited for disadvantaged population groups. Housing costs are the largest expenditure item for private households and affect low-income households in particular. ITEM 367 As a proportion of their income, they spend an average of 9 percentage points more on rent than the average tenant household. Regardless of their income situation, access to adequate housing is even more difficult for tenants with characteristics such as being single parents, families with many children and immigrants. ITEMS 368 AND 370

(15) More residential construction would increase the supply of housing. However, due to the limited availability of land in urban areas, measures are needed to increase the availability of building land in tight housing markets. One example are measures reducing restrictive building regulations in order to increase housing density. In areas with limited potential for densification, additional building plots can be developed by focussing more strongly on greenfield developments outside of the inner cities. ITEM 383 In addition, denser construction on building plots could be stimulated by modifying the property tax to weigh land size more heavily, relative to buildings, than is currently done in most federal states. ITEM 384 Towards this goal, the federal states could adjust their property taxes towards the land value model, which is so far only used in Baden-Wuerttemberg. An additional property tax on undeveloped plots ready for construction (property tax C) could increase incentives to build on those plots. ITEM 385 A DIFFERING OPINION ITEM 423 Last but not least, construction costs should be reduced by facilitating modular and serial construction. In order to achieve this, building standards should be lowered and building regulations should be harmonised between the federal states and partially abolished. ITEMS 386 FF.

(16) In order to utilise the housing stock more efficiently in tight housing markets, barriers to relocation should be reduced. ITEMS 395 FF. Current rent regulation aims to reduce the rent burden in tight housing markets through the rent brake for new rents and lowered caps for increasing existing rents. However, the lowered rent caps reduce the financial incentives to move, as they curb existing rents more than new rents. Rent regulation that is too tight also harbours the risk of reducing private incentives to invest in housing. Due to these negative side effects, lowered rent caps and the rent brake should apply only temporarily and must be accompanied by measures to expand housing supply. ITEM 399 A DIFFERING OPINION ITEM 412 The lowering of rent caps in tight housing markets should be questioned in principle. A stronger weighting of new rents in local rent indices would better reflect market prices and contribute to a smaller gap between new and existing rents. ITEM 400 In the home ownership market, transaction costs could be reduced by lowering the land transfer tax, adjusting regulated notary fees and introducing the ordering-party principle for real estate agent fees for property purchases. ITEMS 403 FF.

(17) The access problem for certain population groups should be solved via social housing policy. Policies tied to the beneficiary (subject-oriented policies) and those tied to construction and housing (object-oriented policies) should complement each other. ITEMS 374 FF. Subject oriented policies such as housing benefits provide low-income households with access to the housing market in a targeted fashion. The main beneficiaries of object-oriented policies such as social housing are households with the same low ability to pay who have additional difficulties to access housing, such as single parents, large families and immigrants. ITEM 374 Social housing therefore fulfils an important supply function for these households. However, as some occupants continue to live in social housing even when their income exceeds the relevant threshold, the instrument is less socially effective than housing benefits. The introduction of a market-oriented misoccupancy levy can increase the accuracy of social housing subsidies. ITEM 411

5. Decarbonising freight transport – modernising transport infrastructure

(18) Freight transport is crucial for a modern economy based on the division of labour. In Germany, freight transport is especially important due to the country's relatively large industrial sector and central geographic location in Europe. ITEMS 425 F. However, freight transport in Germany faces two key challenges: CHART K6 First, the deteriorating condition of the transport infrastructure in Germany BOX 27 increasingly hampers freight transport and economic activity. The anticipated growth in freight transport will further strain the infrastructure. Second, freight transport currently accounts for 8 % of German greenhouse gas (GHG) emissions and must be decarbonised. ITEM 455 Under the European Effort Sharing Regulation (ESR), Germany must meet mandatory European targets for the transport and building sectors.

(19) Germany’s transport infrastructure needs to be modernised and expanded, which requires increased infrastructure spending. CHART K6 TOP ITEMS 491 FF. There is only limited potential to accelerate the decarbonisation of freight transport by shifting from road to rail. Only 6 % of current road freight transport is theoretically suitable for a short-term modal shift. ITEMS 457 FF. Even this potential cannot be realised due to a lack of rail capacity. A far stronger lever for reducing GHG emissions from freight transport is the decarbonisation of road freight transport, which accounts for 98 % of GHG emissions in freight transport. CHART K6 BOTTOM ITEMS 467 FF. To decarbonise trucking, trucks must be converted to alternative powertrains, such as battery electric (BE) or fuel cell electric (FCE) systems.

(20) In the future, users should increasingly finance higher spending on infrastructure, e.g. through a distance-based car toll. ITEM 492 A fixed, longer-term allocation of budget funds to investment promotion agencies could also stabilise infrastructure spending, decrease uncertainty in the planning process and allow to pool planning expertise. ITEM 494 Suitable measures to increase the efficiency and capacity of railways include a Europe-wide introduction of digital automatic coupling, more efficient planning of railway tracks with enough passing tracks and the expansion of European rail corridors. ITEMS 497 FF. The national carbon price, the CO2 component of the truck toll and, in the future, the EU ETS II (EU Emissions Trading System) provide technology-neutral incentives for converting trucks to alternative drive systems. However, the scaling of alternative drive systems requires a corresponding charging and refuelling infrastructure, including grid expansion. ITEMS 505 FF. For a rapid and efficient decarbonisation of road freight transport, policymakers should initially focus on expanding the charging infrastructure for battery-electric trucks. ITEMS 514 FF. A DIFFERING OPINION ITEM 525 FF.

(ECONOMIC) UPTURN FAILS TO MATERIALISE DESPITE IMPROVED GLOBAL ECONOMY

- The German economy is stagnating. Gross domestic product (GDP) has grown by only 0.1 % in real terms over the past five years. One reason is that the German economy is benefitting less from global economic growth than in the past.

- The GCEE expects GDP in Germany to fall by 0.1 % this year. Given weak industry performance and low consumption expenditures. German GDP is expected to grow by only 0.4 % in 2025.

- Consumer price inflation is expected to be 2.2 % this year and 2.1 % next year.

SECURING THE FUTURE OF THE PUBLIC FINANCES

- Future-oriented public spending is not sufficiently prioritised by politicians. This is particularly evident in the areas of transport infrastructure, defence and education.

- The binding nature of such expenditure should be enhanced through institutional arrangements in budgetary and financial planning, which should be tailored to the respective area.

- For the transport sector, an infrastructure fund with its own revenues and, potentially, with limited credit authorisations would be appropriate. Specific minimum spending quotas based on clearly defined indicators are suitable for the areas of defence and education.

ENABLING DIGITAL INNOVATION IN THE FINANCIAL SECTOR; PRESERVE FINANCIAL STABILITY

- The digital transformation in the financial sector promises opportunities such as lower costs for financial services due to process innovation and more competition as well as new financial products.

- Introducing regulatory sandboxes and facilitating the exchange of financial data between big techs, fintechs and banks can foster innovation without creating new systemic risks.

- The digital euro promises improvements in the European payment market and protection against geopolitical risks.

HOUSING IN GERMANY: ADDRESS SHORTAGES AND FACILITATE ACCESS

- The shortage of housing in urban areas is not only a social problem, but also a macroeconomic one, as it inhibits the influx of labour into particularly productive regions.

- The supply of housing can be increased by mobilising potential building land, increasing incentives to build and reducing building costs by harmonising building regulations. Housing could be used more efficiently by reducing social and financial barriers to relocation.

- In social housing policy, subject- and object-oriented support (i.e. subsidies for individuals and for buildings) can meaningfully complement each other, as object-oriented support improves access to housing for disadvantaged groups of people. Their social target accuracy should be improved by means of a misoccupancy levy.

FREIGHT TRANSPORT BETWEEN INFRASTRUCTURE REQUIREMENTS AND DECARBONISATION

- The increasingly poor condition of road and rail infrastructure in Germany is acting as a drag on economic growth and requires higher levels of capital spending.

- Shifting freight transport from road to rail is only possible to a limited extent owing to capacity constraints and largely separate markets for road and rail freight transport.

- To ensure that road freight transport can be decarbonised quickly and efficiently, policymakers should first focus on building the necessary charging infrastructure for battery electric trucks.

Your browser is outdated

Please update your Browser to view this website properly.

You will need at least Internet Explorer 11 to see our interactive charts.

Mozilla Firefox

or alternatively Google Chrome

will provide the best experience for this website.

Update your browser now