EXECUTIVE SUMMARY

Click to share

(1) In this spring report, the German Council of Economic Experts (GCEE) presents its current economic outlook for the years 2024 and 2025. In a second chapter, the GCEE discusses the challenges for freight transport between infrastructure requirements and decarbonisation.

1. Recovery of the German economy is delayed further

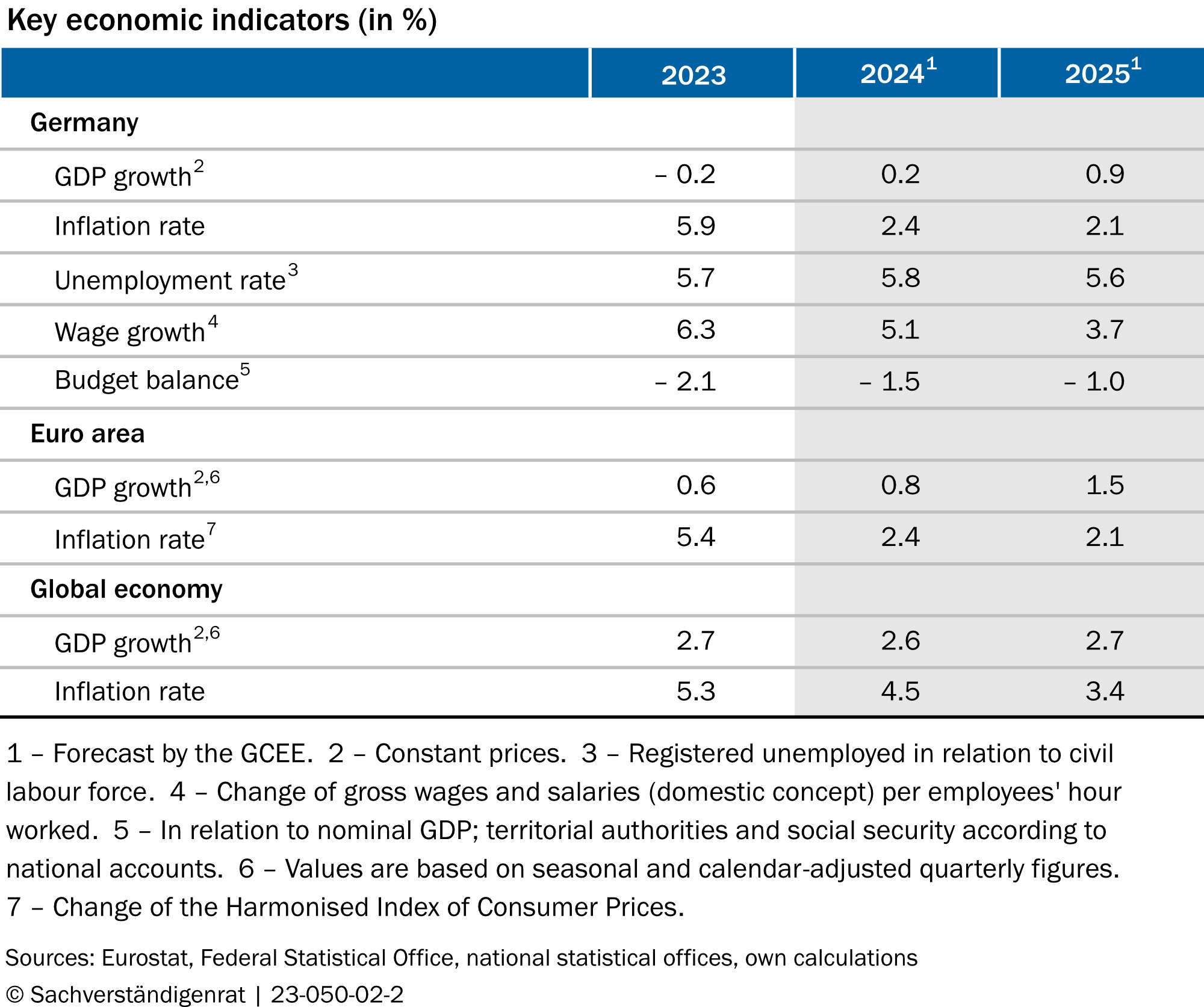

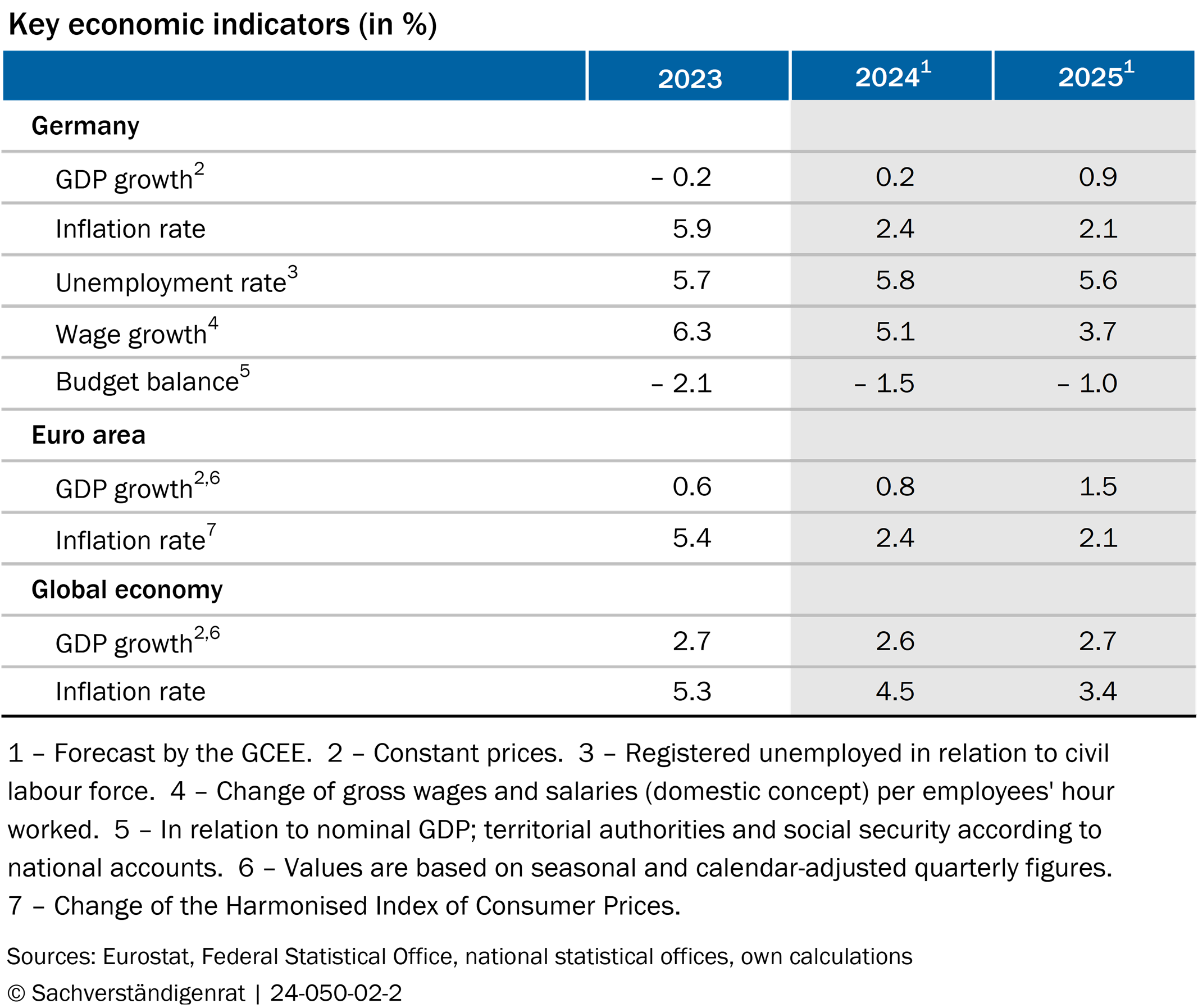

(2) After real gross domestic product (GDP) of the German economy declined by 0.2 % in 2023, the GCEE expects only low GDP growth of 0.2 % in 2024. CHART K1 TOP ITEM 36 However, the German economy is projected to gain some momentum over the course of the year. Inflation is expected to decline, and nominal wages are expected to increase, CHART K1 BOTTOM leading to sustained growth in real incomes and a moderate upturn in private consumption expenditure over the course of 2024. ITEM 38 In 2025, capital formation is also expected to support German GDP growth, which is anticipated to be 0.9 %.

(3) Consumer price inflation in Germany has continued to slow, with significant declines in energy and import prices. Monetary policy is restraining overall economic demand. The GCEE expects that the national consumer price index will increase by 2.4 % in 2024 and 2.1 % in 2025 down from 5.9 % last year. However, rising labor costs are creating domestic price pressures, preventing a faster normalisation of inflation rates. ITEM 47 Core inflation is expected to reach 3.0 % in 2024 and 2.4 % in 2025. Inflation in the euro area has also fallen significantly. ITEM 26 It can therefore be assumed that monetary policy tightening has peaked, with the first interest rate cuts to be expected over the course of the year. ITEM 27 This easing should improve financing conditions throughout the forecast horizon.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

(4) The ongoing war in Ukraine and the conflict in the Middle East pose significant risks to the global economy. ITEM 16 In addition to the risk of energy prices rising again, the future direction of monetary and fiscal policy is uncertain. If inflation in the euro area does not continue to decline as expected, the ECB may delay its first policy rate cuts. ITEM 30 At the same time, additional consolidation may be necessary for the German government budget in 2025. ITEM 48 Both factors could hinder economic recovery, with heightened uncertainty likely to further dampen the investment climate. ITEM 40

2. Freight transport between infrastructure requirements and decarbonisation

(5) Inexpensive, fast and reliable freight transport is crucial for a modern economy with complex value chains, based on the division of labour. It significantly contributes to overall economic productivity. In Germany, freight transport is especially important due to the country's relatively large industrial sector and central geographic location. ITEM 60

Freight transport in Germany faces two key challenges. CHART K2 First, the deteriorating condition of transport infrastructure is already causing capacity bottlenecks and delays, and the anticipated growth in freight transport will further strain the infrastructure. ITEMS 75 FF. Second, freight transport, which accounts for 8 % of German greenhouse gas emissions (GHG emissions), must be decarbonised. ITEMS 80 FF. Although the revised Climate Protection Act no longer specifies annual or sector-specific climate targets, Germany must still meet mandatory European targets for the transport and building sectors under the Effort Sharing Regulation (ESR).

(6) Germany's transport infrastructure needs modernization and expansion, which requires increased infrastructure spending. CHART K2 TOP Greater emphasis on user financing, for example via a mileage-based car toll, could be a solution. ITEM 127 Allocating budget funds to investment promotion agencies on a long-term basis could stabilize infrastructure spending, ensure planning security, and consolidate planning expertise. ITEM 129 Additionally, non-monetary barriers in planning and procurement processes should be eliminated. This includes prioritizing quality over cost in procurement and moving away from medium-sized company requirements if they result in inefficiently small batch sizes.

(7) The potential to shift freight transport from road to rail is limited. ITEMS 93 FF. Only 6 % of current road freight transport is theoretically suitable for a short-term modal shift. However, this potential cannot be realised due to a lack of rail capacity. ITEM 98 A greater modal shift would require a significant increase in the efficiency and capacity of rail transport and an improvement in price competitiveness, for example through a reduction in taxes and levies on traction current. ITEMS 135 FF. Measures to enhance efficiency and capacity include implementing digital automatic coupling across Europe, ITEM 132 improving train path planning with sufficient passing tracks, ITEM 134 and expanding European rail corridors by resolving issues like differences in operating languages. ITEM 135 Separating infrastructure ownership from the rest of the DB Group could also improve rail infrastructure quality and encourage competition between operators. ITEM 137 However, these benefits must be balanced against possible conversion costs and potential losses of economies of scope.

(8) The most significant lever for reducing greenhouse gas emissions (GHG emissions) from freight transport is decarbonizing road freight, which accounts for 98 % of GHG of the freight sector’s emissions. CHART K2 BOTTOM This requires converting trucks to alternative powertrains, such as battery-electric (BE) or fuel-cell (FCE) systems. National carbon pricing, the CO2 component of truck tolls, and the upcoming EU ETS II (EU Emissions Trading System) provide technology-neutral incentives for this transition. ITEMS 85 FF. However, scaling alternative powertrains requires a corresponding charging and refuelling infrastructure, including grid expansion. ITEMS 144 FF. The public sector has a role to play in resolving coordination problems during development. Public funds should be directed toward expanding the charging infrastructure for alternative drive systems to achieve network and scaling effects. ITEM 141

(9) Given the need for decarbonization and limited public funds and planning capacities, government support should initially prioritize developing a nationwide charging infrastructure for BE trucks. ITEMS 149 FF. A DIFFERING OPINION ITEMS 160 FF. First, BE trucks are the most market-ready low-emission technology and are likely to dominate in the near term. ITEM 104 Recent technological advances in batteries and charging have substantially broadened their applications. Synergy effects can be achieved through BE cars and the electrification of other sectors. For instance, charging infrastructure and grid expansion can benefit from renewable energy generation along highways. To improve the regulatory environment for private investment, areas for high-speed charging along highways must be made available, and network capacity for these charging points must be transparently communicated. ITEM 118

Second, only a focus on BE trucks can achieve significant progress towards the decarbonisation of road freight by 2030. ITEM 106A DIFFERING OPINION ITEMS 168 FF. While green hydrogen availability remains uncertain in the near term, BE trucks can immediately reduce emissions with the current electricity mix. Additionally, hydrogen has competing applications, especially in industries where processes are challenging to electrify. A DIFFERING OPINION ITEMS 179 FF.

Third, BE trucks serve as the technical basis for FCE trucks. A focus on BE trucks won't preclude future adoption of FCE trucks for long-distance freight if necessary. ITEM 156A DIFFERING OPINION ITEMS 173 FF. Such applications are niche, however, and don't justify a nationwide hydrogen refuelling infrastructure. Instead, mobile or private refuelling stations, or synthetic fuels, can meet these needs. A DIFFERING OPINION ITEMS 175 FF.

(10) The ramp-up of low-emission road freight transport should be coordinated across Europe. The EU AFIR (Alternative Fuels Infrastructure Regulation) already mandates the development of parallel charging and refuelling infrastructures for both BE trucks and FCE trucks by 2030. BOX 18 The interim evaluation in late 2024 provides Germany with an opportunity to coordinate with other EU member states to jointly reassess the market potential and requirements for alternative fuel infrastructure regulated by AFIR at the European level. ITEM 159A DIFFERING OPINION ITEMS 181 FF.

RECOVERY OF THE GERMAN ECONOMY IS DELAYED FURTHER

- In 2024, real income growth is likely to slowly stimulate private consumption expenditure and thus the German economy. Capital formation is also expected to pick up slightly in 2025.

- The GCEE expects Germany's price-adjusted gross domestic product to increase by just 0.2 % this year and by 0.9 % in 2025. Consumer price inflation is expected to be on an annual average of 2.4 % and 2.1 % respectively.

- The outlook is subject to significant risks due to the uncertainty surrounding geopolitical developments as well as public finance and economic policy.

FREIGHT TRANSPORT BETWEEN INFRASTRUCTURE REQUIREMENTS AND DECARBONISATION

- The deteriorating condition of the road and rail infrastructure hampers economic development in Germany. At the same time, freight transport needs to be decarbonised.

- To swiftly and efficiently decarbonise road freight transport, government support should initially prioritise expanding a nationwide charging infrastructure for battery-electric trucks.

- Shifting freight transport from road to rail is limited by the rail network's lack of capacity. It is thus crucial to modernise and expand the rail infrastructure.

Your browser is outdated

Please update your Browser to view this website properly.

You will need at least Internet Explorer 11 to see our interactive charts.

Mozilla Firefox

or alternatively Google Chrome

will provide the best experience for this website.

Update your browser now